The Most Important Number in Philippine Real Estate Right Now

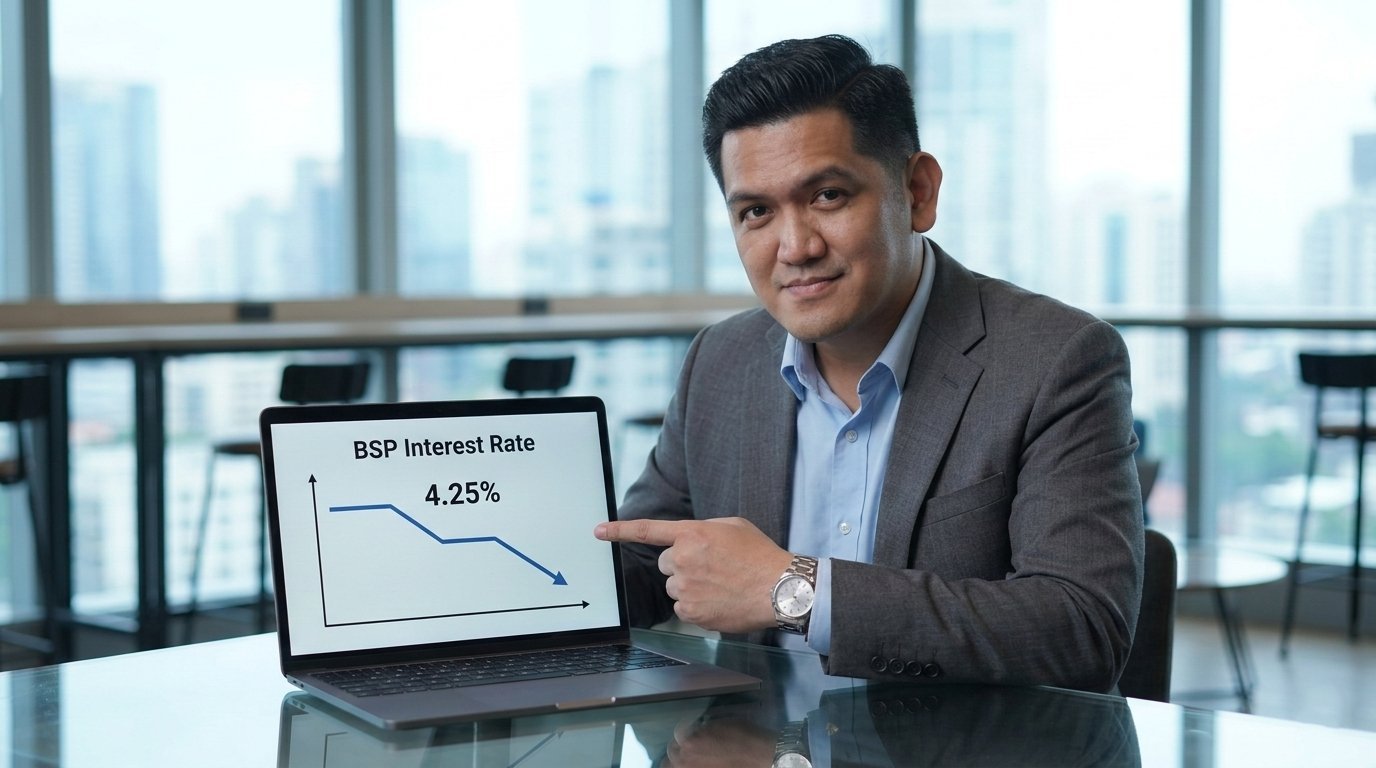

The Bangko Sentral ng Pilipinas has been cutting rates aggressively. Since August 2024, the BSP has reduced its benchmark overnight reverse repurchase rate by a cumulative 225 basis points — from 6.5% down to 4.25% as of February 2026. That's one of the most significant monetary easing cycles in recent Philippine history, and it matters enormously for property buyers.

But here's what the headlines don't always tell you: the banks haven't passed on the full cut. Bloomberg reported in November 2025 that despite the BSP slashing its key rate by nearly two percentage points, home loan rates at major Philippine banks had barely budged. As of early 2026, the average mortgage rate from major banks ranges from about 7% to 10%, depending on the lender, loan term, and borrower profile. Some digital lenders are now advertising as low as 5.99% for qualified borrowers. Pag-IBIG, as always, remains the most affordable option for eligible buyers — with rates as low as 3% for the first five years under its Affordable Housing Program.

Why the Gap Exists — and Why It Will Close

Banks are cautious institutions. They move slowly after rate cuts, partly because their cost of funds doesn't reprice immediately and partly because lending margins serve as buffers against default risk. The transmission lag between BSP rate cuts and actual mortgage rate reductions typically runs three to six months. Colliers Philippines research director Joey Bondoc noted that the full effect of rate cuts was expected to be felt by mid-2025 — and by early 2026, there are signs of gradual movement, with rates trending modestly lower across most lenders. Nook, the Philippines' first dedicated mortgage broker, is now listing starting rates of 5.99% for well-qualified borrowers — a figure that would have seemed optimistic eighteen months ago.

What This Means for Pre-Selling Buyers Specifically

Here's the angle that most coverage misses: if you're buying pre-selling today, you won't be drawing down your bank loan for another two to four years. The rate environment at turnover — not today's rates — is what determines your actual financing cost. The BSP's own projections for 2026 and 2027 put inflation firmly within the 2%–4% target band. The easing cycle is nearing its end, but there's no credible scenario for aggressive rate hikes in the near term. Buyers who lock in a pre-selling price today and arrange bank financing at turnover may find themselves doing so into a more favorable rate environment than currently exists.

This is exactly the logic that makes pre-selling the preferred entry strategy for buyers with a 3–5 year horizon. Add lower entry pricing and flexible equity payment terms to an improving rate outlook at the point of bank financing, and the arithmetic gets compelling. Contact us to walk through the specific payment structure and financing options for any of the projects we represent.